The Strategic Unraveling of XLMedia

A Promising Start in Digital Media

Founded in 2008 as Webpals Marketing Systems Ltd. and rebranded as XLMedia in 2013, the company carved a niche in the competitive iGaming and sports betting affiliate space. Listed on the London Stock Exchange’s AIM market (XLM), XLMedia built a portfolio of owned-and-operated sites like SportsBettingDime and Saturday Down South, alongside media partnerships, to connect engaged audiences with advertisers in regulated markets. By 2018, its share price peaked above 200p, reflecting optimism about its growth in the burgeoning U.S. sports betting market post-PASPA repeal. Yet, beneath this success lay vulnerabilities that would precipitate its downfall.

Asset Sales Signal Strategic Retreat

By 2024, XLMedia’s trajectory shifted dramatically. Facing mounting competitive pressures and financial strain, the company executed two pivotal asset sales. In March 2024, it sold its European and Canadian sports betting and gaming assets, including Freebets.com, to Gambling.com Group for up to $42.5 million ($37.5 million upfront, $5 million earnout). In October 2024, it divested its North American portfolio—key sites like Elite Sports NY and Saturday Tradition—to Sportradar AG for up to $30 million ($20 million upfront, $10 million earnout). These deals, totaling a potential $72.5 million, were framed as efforts to “unlock shareholder value” but effectively stripped XLMedia of its core operations, leaving it as an AIM Rule 15 cash shell by late 2024.

Financial Struggles and Earnout Shortfalls

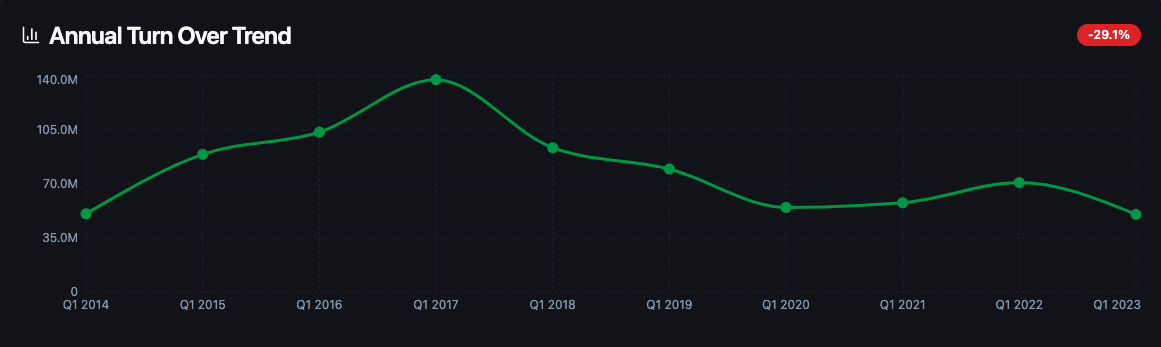

The asset sales exposed XLMedia’s financial fragility. The company reported a 23% revenue decline from $65.7 million in 2022 to $50.3 million in 2023, culminating in a $15 million operating loss in FY2024 before impairments. The anticipated earnouts from the sales underperformed, with only $1 million received from Sportradar (versus $10 million expected) due to sluggish U.S. revenue growth, and an estimated $3–5 million total from Gambling.com. With just $35 million in cash by Q1 2025 and a skeleton crew of seven employees (down from 146 in 2023), XLMedia lacked the resources to rebuild or pivot effectively.

Disclaimer: This article and its accompanying images may have been enhanced using AI tools to ensure smoother content delivery and visual appeal.

Why XLMedia Chose Liquidation

Competitive Pressures in a Consolidating Market

The iGaming affiliate sector has grown increasingly cutthroat, with larger players like Better Collective (market cap ~€1.5 billion in 2024) and Catena Media dominating through scale, diversified portfolios, and robust operator relationships. XLMedia, with a market cap of ~£25 million at its 2024 peak, struggled to compete. Rising customer acquisition costs in the U.S., coupled with stricter regulations in markets like the UK, squeezed affiliate margins. Google’s algorithm changes further eroded traffic to XLMedia’s SEO-dependent sites, undermining its revenue model.

A Cash Shell with No Viable Path Forward

Post-divestitures, XLMedia’s status as a cash shell imposed a six-month deadline under AIM rules to pursue a reverse takeover or new business plan. The board explored options but found no suitable acquisition targets, likely due to high valuations in the affiliate space and XLMedia’s diminished bargaining power. Rebuilding its sports and gaming portfolio or pivoting to new verticals like personal finance—where it had previously faltered with brands like MoneyUnder30—required capital and expertise the company no longer possessed. Continuing as a standalone entity risked further value erosion, as evidenced by its share price collapse from 200p in 2018 to ~10p by 2024.

Prioritizing Shareholder Returns

The board’s decision to liquidate was driven by a fiduciary duty to maximize shareholder value. Two tender offers in 2025—£14 million in January (11.5p/share, 46% of shares) and £11 million in April (11p/share, 71% of remaining shares)—distributed £25 million at premiums of 16–24% to the prevailing share price. Trading was suspended on May 14, 2025, and shares were delisted from AIM on June 18, 2025. Liquidation, with potential for further distributions (10p/share estimated surplus), offered a clearer path to value than a speculative turnaround in a consolidating industry.

Lessons for iGaming Leaders: A Critical Perspective

The Perils of Insufficient Scale

XLMedia’s demise underscores a brutal reality for iGaming affiliates: scale is non-negotiable. Smaller players face relentless pressure from well-capitalized competitors who can absorb rising acquisition costs, navigate regulatory complexities, and invest in proprietary technology. XLMedia’s reliance on a narrow portfolio and SEO-driven traffic left it vulnerable to market shifts, a warning for affiliates who fail to diversify revenue streams or build defensible moats. The company’s inability to scale its U.S. operations, despite early mover advantage post-PASPA, highlights the need for strategic agility and deep financial reserves.

Regulatory and Market Headwinds Demand Adaptability

The iGaming landscape is no longer a land of opportunity for all. Stricter regulations—state-by-state U.S. licensing, UK advertising restrictions—have raised compliance costs and favored operators with in-house marketing or partnerships with mega-affiliates. XLMedia’s failure to adapt its affiliate model to these realities, coupled with its dependence on volatile traffic sources, sealed its fate. Industry leaders must prioritize regulatory foresight and flexible business models to survive consolidation waves

Strategic Missteps and Missed Opportunities

Critics argue XLMedia’s board was too quick to dismantle the company rather than pursue a bolder reinvention. A reverse takeover or targeted acquisitions in emerging niches (e.g., esports betting, Web3 gaming, Prediction…) could have offered a lifeline, albeit with risks. The decision to sell assets to competitors like Gambling.com and Sportradar, while lucrative in the short term, handed rivals XLMedia’s market share and relationships. This raises questions about whether the board undervalued the company’s potential or lacked the vision to navigate a path forward. For iGaming leaders, XLMedia’s story is a reminder to balance immediate shareholder pressures with long-term strategic ambition.

The Broader Implications for the Affiliate Ecosystem

The liquidation of XLMedia reflects a broader trend of consolidation in the iGaming affiliate space. As larger players acquire smaller ones—evidenced by Gambling.com and Sportradar’s purchases—mid-tier affiliates face existential threats. The industry is shifting toward a winner-takes-most dynamic, where only those with scale, technological innovation, or niche dominance can thrive. For iGaming leaders, XLMedia’s collapse signals the need to invest in proprietary platforms, diversify into adjacent verticals, and forge stronger operator partnerships to avoid becoming acquisition targets or fading into irrelevance.

Is that path that Catena Media will be following …?